17 May 2026

Bank Account Integrations Reveal APR Differences in Vehicle and Home Refinancing

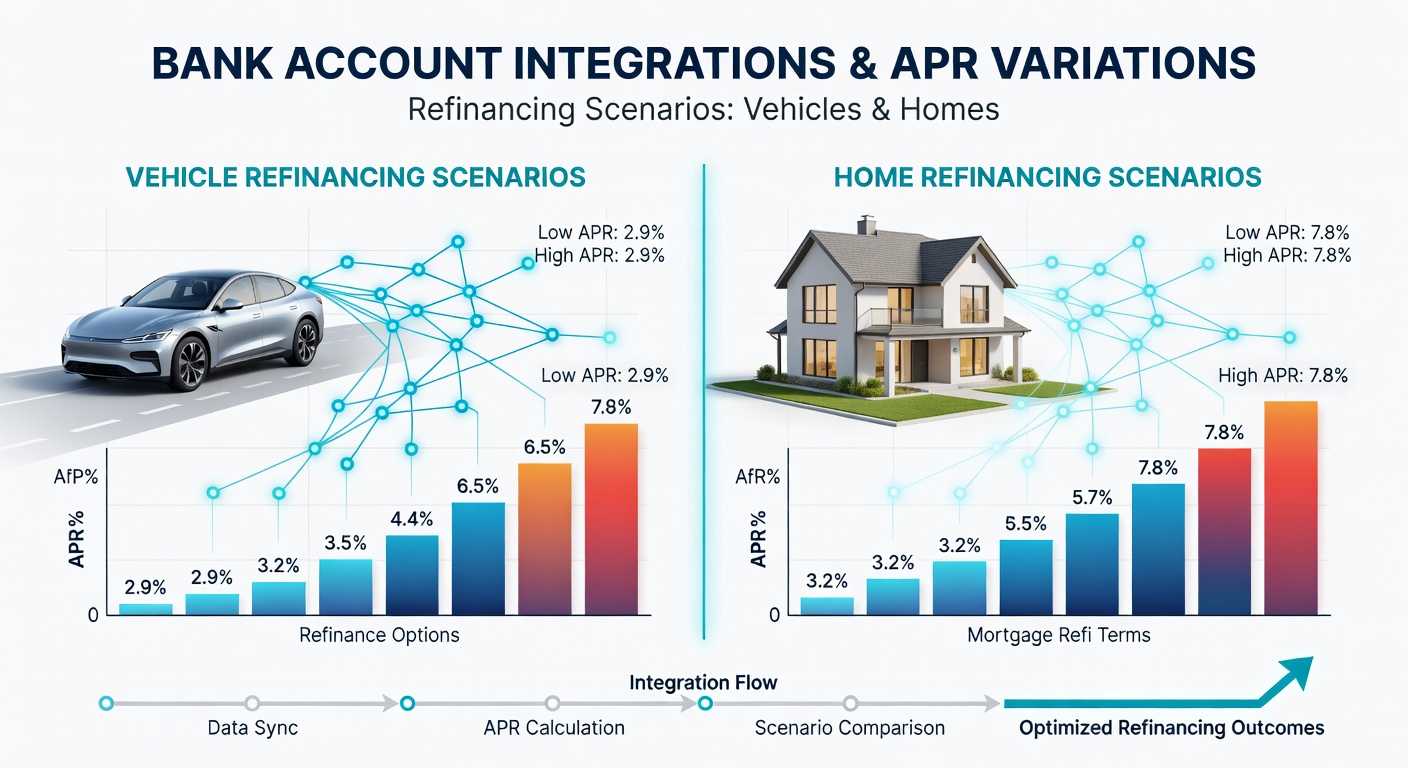

Bank account integrations now connect directly with refinancing platforms, allowing users to view live APR quotes for both vehicle loans and home mortgages within a single dashboard, and these connections have grown more sophisticated by May 2026. Financial institutions link checking and savings accounts to credit monitoring services, which then pull real-time data on outstanding balances, payment histories, and current interest rates to generate personalized refinancing estimates. Observers note that such seamless access highlights clear distinctions in APR structures, since vehicle refinancing typically carries higher rates than home loan options due to shorter terms and depreciating collateral values.

Research from multiple banking networks indicates that auto refinancing through integrated accounts often surfaces APR ranges between 4.8 and 7.2 percent for borrowers with strong credit profiles, whereas home mortgage refinances display averages from 3.1 to 4.9 percent under similar conditions. These variations emerge because lenders apply different risk models, with vehicle loans factoring in mileage, model year, and residual value assessments that elevate APR calculations. In contrast, home refinancing benefits from property appraisals that provide stable collateral, which tends to compress rate spreads even when market conditions fluctuate.

Integration Mechanics Across Lending Types

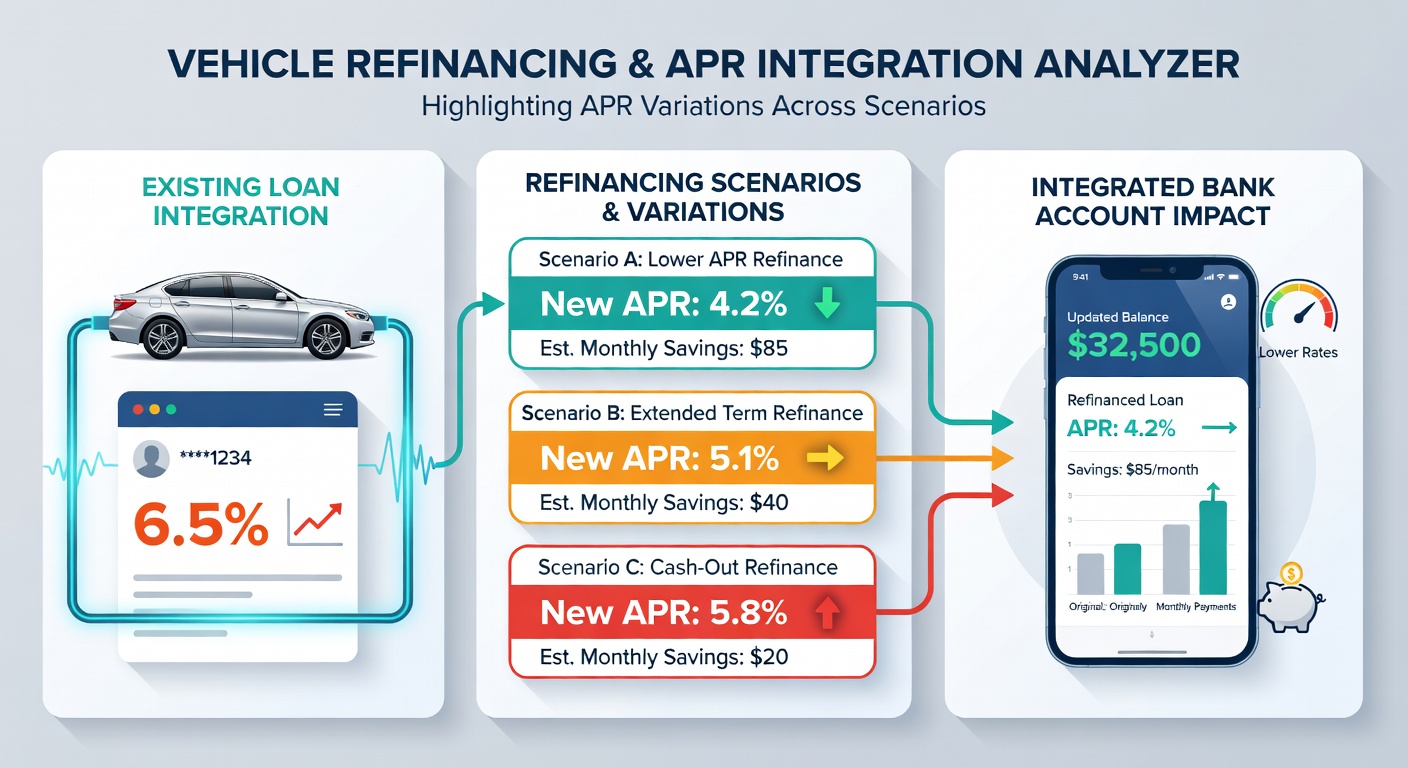

Modern banking apps use secure API connections to aggregate loan data from external providers, and this process enables side-by-side APR displays that update daily based on Federal Reserve benchmark adjustments. Users authorize account access once, after which algorithms scan transaction patterns to suggest optimal refinancing windows for either cars or residences. Data shows that platforms incorporating these integrations reduce quote generation time from days to minutes, while simultaneously flagging how credit utilization ratios influence final APR offers in each category.

Vehicle Refinancing Patterns

Vehicle refinancing scenarios benefit particularly from bank integrations because they allow instant verification of loan-to-value ratios through linked statements, and this verification often reveals APR premiums tied to shorter repayment periods. Lenders typically structure auto offers around five-to-seven-year terms, which results in elevated rates compared to longer-duration products. Figures from industry reports reveal that borrowers refinancing trucks or SUVs encounter slightly wider APR bands than those handling sedans, owing to differences in depreciation curves and insurance requirements that feed directly into pricing engines.

Home Mortgage Refinancing Dynamics

Home refinancing integrations pull property records and equity calculations into the same interface that handles vehicle loans, creating a unified view where APR variations become immediately visible. Mortgage products usually feature fixed-rate structures that lock in lower percentages over fifteen-to-thirty-year horizons, and bank systems highlight these advantages by contrasting them against floating auto rates. According to Federal Reserve consumer credit data, average mortgage refinance APRs remained anchored near 3.7 percent through early 2026, while parallel vehicle figures climbed above six percent when credit scores dipped below 720.

European Central Bank analyses further illustrate how regional rate environments affect these integrations, since eurozone mortgage refinances often post even tighter APR spreads when property values appreciate steadily. Observers note that integrated platforms now include stress-test simulations, showing how an increase in benchmark rates would widen the gap between vehicle and home refinancing costs over time.

Comparative APR Influences in Practice

Turnout from case studies demonstrates that borrowers using integrated accounts frequently discover APR savings of 1.5 to 2.8 percentage points when moving existing vehicle debt into newer terms, although such gains depend heavily on timing relative to credit bureau updates. Home scenarios produce steadier but smaller reductions because baseline mortgage rates already sit lower, and integration tools emphasize total interest paid across full loan lifecycles rather than headline percentages alone. What's interesting is how these systems flag ancillary fees that indirectly alter effective APRs, such as origination costs on autos versus appraisal expenses on homes.

Bank of Canada research publications indicate that cross-border borrowers see additional layers of variation when refinancing involves currency conversions, yet domestic integrations still dominate usage patterns. Those who monitor these dashboards regularly identify seasonal dips, particularly around tax filing periods when liquidity improves and lenders compete more aggressively on both vehicle and property products.

Conclusion

Bank account integrations continue to sharpen visibility into APR differences between vehicle and home refinancing, delivering side-by-side metrics that reflect distinct risk profiles and term structures. As of May 2026, these tools have become standard features in major financial apps, enabling precise comparisons grounded in live data feeds. Continued refinement of API connections promises even more granular breakdowns, helping users align refinancing choices with their specific collateral and repayment timelines.