2 Jun 2026

Calculator Tools Spot APR Shifts When Deposit Accounts Link Student Debt Payoffs to Future Auto and Home Borrowing Paths

Deposit account data feeds directly into specialized calculator platforms that model how clearing student loan balances alters projected annual percentage rates for subsequent vehicle and property financing; these tools pull transaction histories and balance patterns from linked checking and savings accounts to generate scenario-based forecasts. Observers note that platforms integrate real-time deposit flows with payoff simulations, allowing users to see how consistent account activity influences credit profiles once education debt drops away. Financial institutions report that deposit account linkages provide context beyond standard credit scores by revealing cash flow stability and savings patterns that lenders review during auto and mortgage underwriting processes. Data from June 2026 shows increased adoption of these integrated calculators as borrowers seek to map post-student-debt borrowing costs with greater precision. Researchers at institutions tracking consumer credit indicate that account activity metrics often correlate with rate adjustments of 0.25 to 0.75 percentage points across secured loan products.

Deposit account data feeds directly into specialized calculator platforms that model how clearing student loan balances alters projected annual percentage rates for subsequent vehicle and property financing; these tools pull transaction histories and balance patterns from linked checking and savings accounts to generate scenario-based forecasts. Observers note that platforms integrate real-time deposit flows with payoff simulations, allowing users to see how consistent account activity influences credit profiles once education debt drops away. Financial institutions report that deposit account linkages provide context beyond standard credit scores by revealing cash flow stability and savings patterns that lenders review during auto and mortgage underwriting processes. Data from June 2026 shows increased adoption of these integrated calculators as borrowers seek to map post-student-debt borrowing costs with greater precision. Researchers at institutions tracking consumer credit indicate that account activity metrics often correlate with rate adjustments of 0.25 to 0.75 percentage points across secured loan products.Deposit Account Integration Mechanics

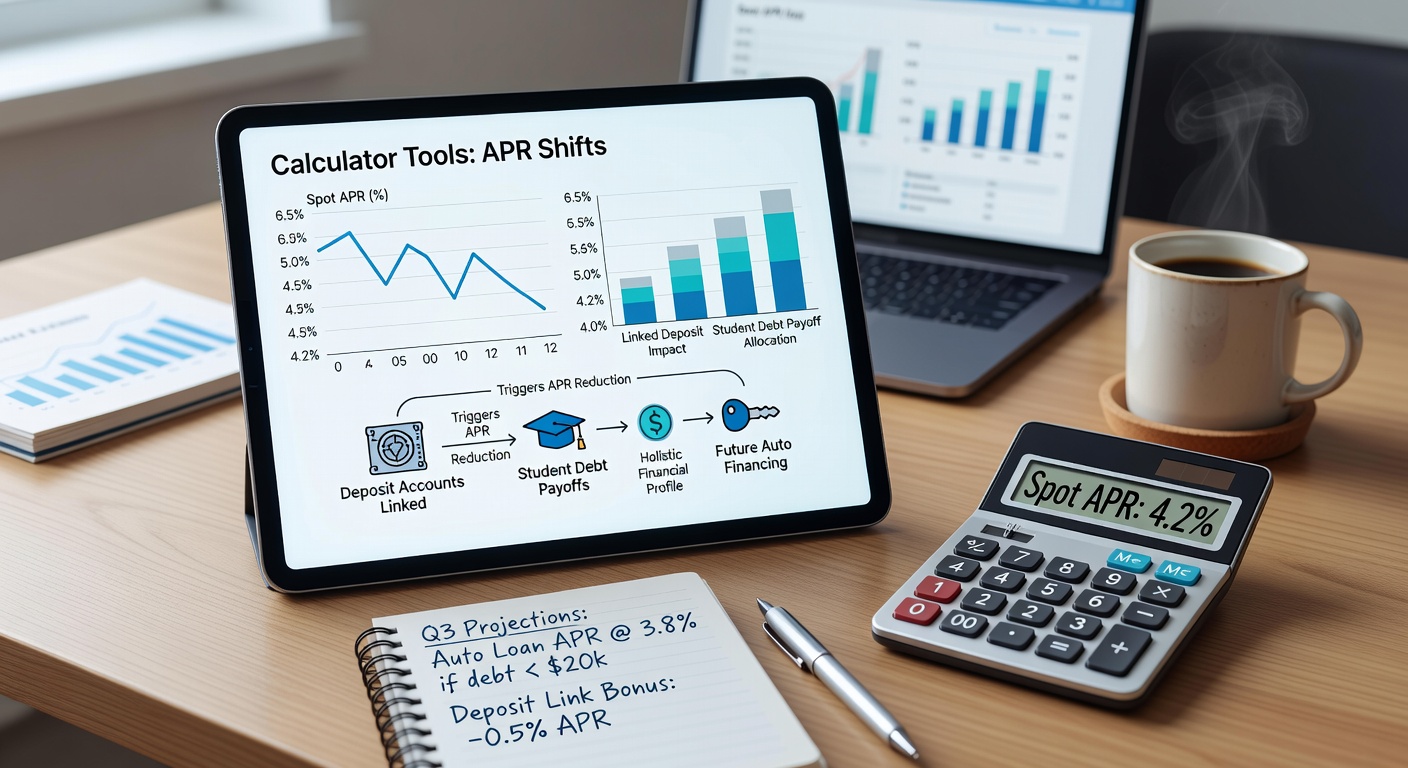

Calculators connect to deposit accounts through secure APIs that extract average balances, deposit frequency, and outflow trends without exposing full transaction details to external parties. This linkage enables models to simulate how accelerated student debt reduction frees monthly cash flow, which in turn projects improved debt-to-income ratios for future auto and home loan applications. Studies conducted by academic centers in Canada demonstrate that borrowers maintaining steady deposit patterns achieve measurable APR reductions when calculators incorporate six months of account data prior to payoff completion.

Platform algorithms weigh deposit account longevity and minimum balance thresholds alongside payoff amounts to generate tiered APR estimates. Those who've examined multiple scenarios often discover that early payoff combined with sustained account activity produces narrower rate spreads for vehicle financing compared to mortgage products, where property valuation factors dominate.

APR Projection Patterns Across Borrowing Types

Outputs from these calculators highlight distinct rate trajectories once student obligations clear. Auto loan projections frequently show sensitivity to deposit account utilization rates because lenders treat consistent savings deposits as indicators of repayment reliability. Home borrowing estimates incorporate broader variables yet still register shifts when calculators factor freed cash flow into long-term qualification models. Figures released by the Federal Reserve in early 2026 illustrate average APR declines of 0.4 percentage points for auto loans among borrowers who cleared education debt within the prior calendar year while maintaining deposit account linkages.

What's interesting is how the same input sets produce different outcomes depending on whether the model prioritizes short-term auto financing or extended mortgage horizons. One study revealed that deposit account data strengthens auto loan projections more noticeably because shorter loan terms amplify the impact of improved cash flow metrics. Mortgage calculators, by contrast, spread the effect across decades, resulting in subtler but cumulative rate advantages when account linkages remain active.

June 2026 Market Context

Market conditions in June 2026 reflected steady student debt payoff volumes alongside elevated demand for vehicle and property financing. Calculator usage spiked during this period as users tested scenarios that incorporated deposit account metrics to anticipate rate environments shaped by evolving monetary policy. Government statistical agencies in Australia recorded parallel trends, noting that borrowers who linked accounts before completing education debt payoffs encountered more favorable pre-qualification ranges for both auto and home products.

Industry reports indicate that platforms updated their models in spring 2026 to account for regulatory changes affecting how deposit histories factor into credit assessments. These adjustments allowed calculators to generate more granular APR forecasts that reflect regional lending standards across North American and European markets.

Practical Application Examples

Borrowers who run multiple calculator iterations before initiating student debt payoffs frequently identify optimal timing windows that align account activity peaks with loan applications. Case examples documented by research firms show individuals who maintained deposit account balances above platform thresholds achieving projected APR advantages of up to 0.6 percentage points on subsequent auto financing. Similar patterns emerge in home lending pathways where calculators demonstrate how payoff sequencing influences mortgage rate lock options.

Platforms continue to refine their data inputs to capture seasonal deposit fluctuations that affect projection accuracy. Those monitoring these tools report that quarterly updates incorporating fresh June 2026 lending data improve forecast reliability for users planning multi-year borrowing sequences.

Conclusion

Calculator platforms that connect deposit accounts to student debt payoff modeling deliver targeted APR projections for future auto and home borrowing by synthesizing account behavior with credit variables. Continued refinement of these tools through 2026 supports more precise financial planning across multiple loan categories while maintaining focus on verifiable data inputs from linked accounts.