26 May 2026

Charting Cross-Borrowing Pathways: How Integrated Calculators Uncover APR Edges When Moving Funds Between Credit Lines and Asset-Based Debts

Financial tools that connect multiple borrowing accounts now allow users to map potential shifts of funds from revolving credit lines into secured asset-based debts and back again while highlighting APR variations that standard comparisons often miss. These integrated calculators pull live data on outstanding balances, interest structures, and repayment schedules so that patterns emerge when funds cross between unsecured credit facilities and collateral-backed obligations such as home equity products or equipment financing. Observers note that the process reveals incremental savings opportunities that arise only when all accounts feed into a single analytical view rather than remaining siloed.

Data from May 2026 shows household borrowing patterns continuing to favor strategic movement between credit lines and asset-based facilities when rate differentials exceed typical thresholds. Integrated platforms aggregate information across lenders, apply standardized APR formulas that include fees, and project monthly cash-flow impacts over multi-year horizons. Researchers at several institutions have documented that such projections frequently identify edges of 1.5 to 3 percentage points that surface only after simultaneous modeling of both debt categories.

Mechanics of Integrated Calculators in Cross-Borrowing Scenarios

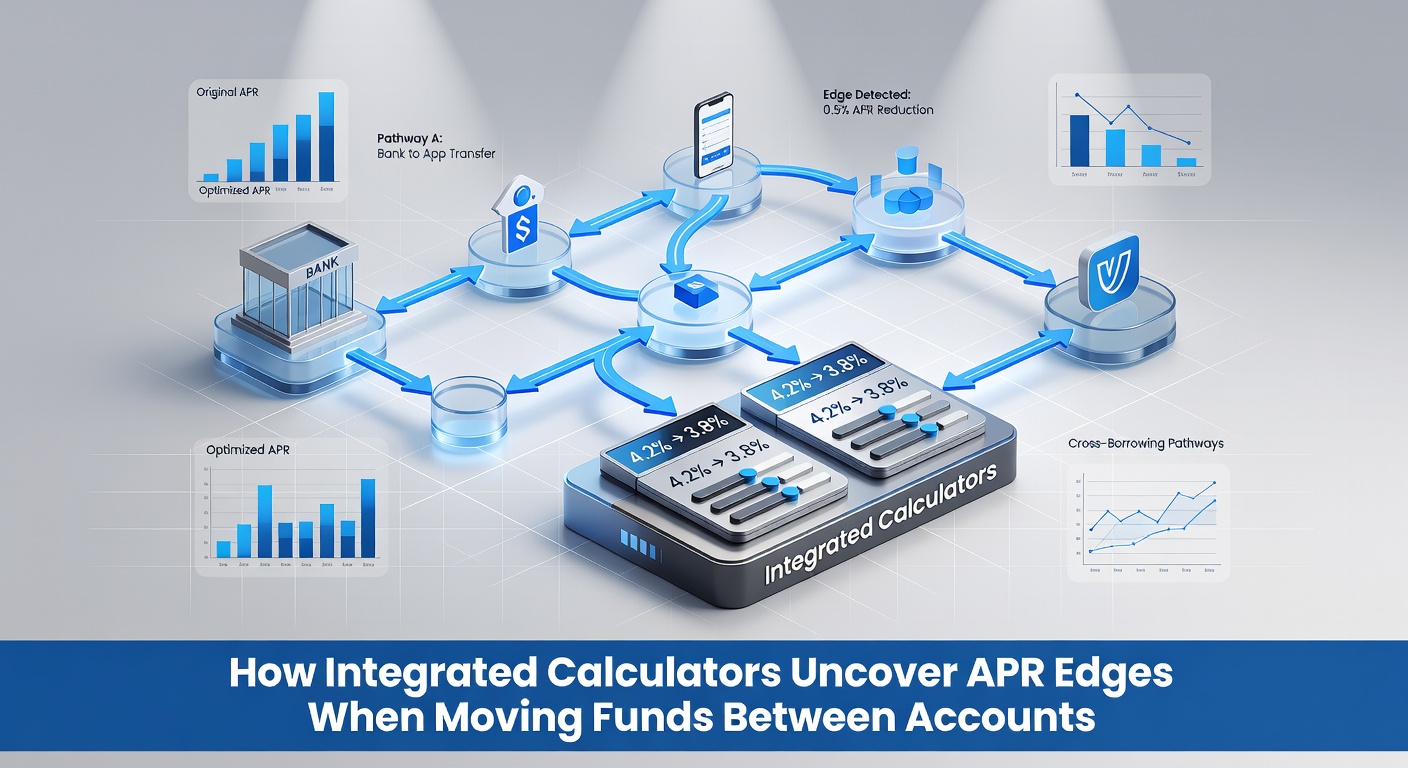

Calculators designed for cross-borrowing operate by linking application programming interfaces from banks and credit unions so that real-time balances update automatically inside one interface. Once connected, the software applies uniform APR calculations that factor origination fees, late-payment penalties, and any introductory rate periods that may differ between credit lines and asset-based loans. Users input target transfer amounts and the tool simulates outcomes across varying time frames while adjusting for changes in collateral values that affect secured debt rates.

One study released in early 2026 examined several thousand anonymized user sessions and found that the most common pathway involved moving portions of revolving balances onto asset-based lines when equity positions allowed lower effective rates. The same analysis indicated that reverse movements, from secured debt back to credit lines, occurred less frequently yet produced measurable advantages when asset values declined or when borrowers needed flexibility not permitted under strict collateral covenants.

APR Components That Calculators Isolate During Transfers

Standard APR disclosures combine interest charges with certain fees yet often omit dynamic elements that appear only during actual fund movements. Integrated calculators isolate these components by recalculating the blended rate after each simulated transfer and displaying side-by-side comparisons that update instantly. They also track how remaining credit limits on revolving accounts change once balances decrease, a factor that influences future borrowing capacity and overall cost structures.

Figures released by the Federal Reserve in spring 2026 indicated that average APR spreads between unsecured credit lines and asset-based products had widened modestly since the prior year, creating more frequent windows where transfers produced net savings. Calculators surface these windows by running sensitivity analyses on variables such as expected interest-rate movements and projected changes in household income that could affect qualification for lower-rate secured facilities.

Practical Pathways and Observed Outcomes

Borrowers who route funds from credit lines into asset-based debts typically begin by using the calculator to confirm that collateral coverage meets lender requirements and that the resulting APR reduction offsets any closing costs. The tool then generates amortization schedules that illustrate cumulative interest paid under both the original and proposed structures, allowing direct comparison of total outlays over identical time periods. When the projected savings exceed a preset threshold, the platform flags the pathway for further review.

Reverse pathways, shifting funds from asset-based debts back onto credit lines, appear when borrowers anticipate short-term liquidity needs or when collateral valuations drop enough to raise secured rates. Calculators quantify these scenarios by modeling the impact of higher revolving rates against the preservation of asset equity and the avoidance of potential foreclosure triggers tied to secured agreements. European Central Bank lending statistics from the first quarter of 2026 showed similar patterns emerging across several member states where integrated tools gained wider adoption.

Data Inputs and Modeling Accuracy

Accuracy depends on the breadth of connected accounts and the frequency with which rates update within the calculator environment. Platforms that refresh daily from multiple sources produce projections that align more closely with actual outcomes once transfers occur. Users who maintain complete linkages across credit cards, lines of credit, and secured loans report fewer discrepancies between modeled and realized APR savings compared with those who enter data manually.

Additional variables such as tax treatment of interest on certain asset-based debts and the effect of credit-score changes following balance movements also factor into the calculations. These elements receive automatic weighting when the software draws from verified account histories rather than relying solely on user-supplied estimates.

Conclusion

Integrated calculators have become central to identifying APR advantages when funds move between credit lines and asset-based debts because they consolidate disparate data streams into unified projections. By May 2026 these tools routinely highlighted transfer opportunities that surface only when all relevant accounts operate inside the same analytical framework. Continued expansion of account connectivity and more granular fee disclosures are expected to refine the precision of such cross-borrowing analyses further in subsequent periods.