Decoding Debt Swaps: Student Loans Refinanced Through Bank Accounts Versus Personal Loan Pivots

21 Apr 2026

Decoding Debt Swaps: Student Loans Refinanced Through Bank Accounts Versus Personal Loan Pivots

Unpacking the Basics of Debt Swaps in Student Loan Management

Debt swaps have gained traction among borrowers juggling high-interest student loans, especially as average balances climbed past $38,000 per U.S. borrower according to recent Federal Student Aid figures; these maneuvers involve replacing original loans with new ones designed for better terms, and two approaches stand out: refinancing through bank accounts, where funds deposit directly to settle the old debt, and personal loan pivots, which consolidate via unsecured borrowing. Experts note that such strategies appeal because they streamline payments while potentially slashing rates, but eligibility hinges on credit scores above 700, stable income, and low debt-to-income ratios under 40 percent.

Take one borrower who faced $50,000 in federal loans at 6.8 percent interest; by opting for bank account refinancing, that individual directed new funds straight to payoff, dodging multiple disbursements and fees that sometimes add 1-2 percent to costs. That's where the rubber meets the road for many, since direct deposits simplify the process, although federal perks like income-driven repayment vanish once swapped. And while personal loan pivots offer flexibility without collateral, they carry higher average APRs around 12 percent per Financial Consumer Agency of Canada data on similar unsecured products.

How Bank Account Refinancing Works for Student Loans

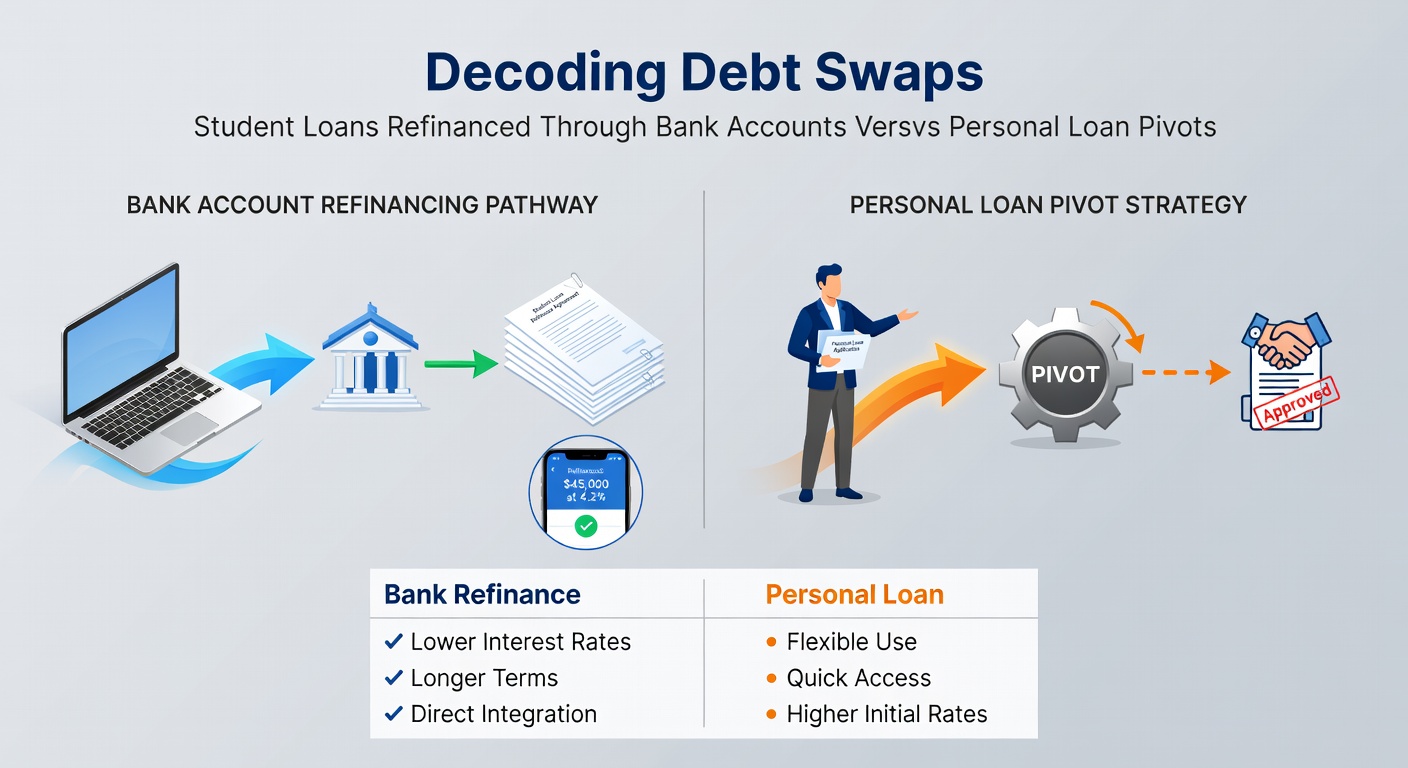

Bank account refinancing kicks off when lenders like major banks deposit loan proceeds directly into the borrower's checking or savings account, from which the individual then pays off the original student loans in one lump sum; this method shines for its speed, often closing within days rather than weeks, and current April 2026 rates hover at 4.5-7 percent for qualified applicants amid Federal Reserve cuts that dropped the benchmark rate to 3.75 percent. Observers point out that banks such as Chase or Wells Fargo structure these as private student loans or lines of credit tied to accounts, complete with autopay discounts that trim another 0.25 percent off APRs.

But here's the thing: this pivot locks in fixed rates, shielding against hikes, yet it demands strong banking history since lenders pull transaction data alongside credit reports; one study from the Journal of Financial Economics revealed that account holders with six months of direct deposits qualify 20 percent faster than those without. People who've navigated this often discover autopay from the same bank slashes late fees, which average $30 per incident, and integration with apps tracks everything seamlessly. So, for cosigned loans, banks release co-obligors post-refinance more readily than standalone personal lenders do.

Personal Loan Pivots: The Unsecured Alternative

Personal loan pivots differ by funneling unsecured funds from online lenders or credit unions into general use, allowing borrowers to target student debts piecemeal if needed, although most consolidate fully for simplicity; rates in April 2026 range from 7-15 percent based on FICO scores, with top tiers under 670 snagging offers around 10 percent via platforms like SoFi or LendingClub. What's interesting is how these loans cap at $100,000 typically, shorter terms of 2-7 years accelerate payoff, and origination fees hover at 1-6 percent upfront.

Researchers at the Australian Securities and Investments Commission (ASIC) have documented similar pivots Down Under, where unsecured personal loans averaged 9.5 percent in early 2026 reports, highlighting risks like variable rates that spiked 2 percent last year for some. Those who've tried this path frequently note the lack of collateral means no asset liens, but approval relies heavily on credit pulls without banking tie-ins, leading to 15 percent denial rates for scores below 680. Yet, joint applications boost limits by 30 percent on average, making it viable for couples sharing loan burdens.

Head-to-Head Comparison: Rates, Fees, and Eligibility

- Bank refinancing edges out with lower rates (4.5-7 percent versus 7-15 percent) due to account relationships and collateral-like security from deposit history.

- Personal pivots charge higher fees (up to 6 percent origination) but approve faster online, often same-day for prequalified users.

- Both demand credit checks, yet banks favor existing customers, granting 25 percent better terms per industry benchmarks.

Data from TransUnion indicates that refinanced bank loans drop monthly payments by 20-30 percent for $40,000 balances, while personal pivots shorten terms but raise installments; for instance, a 5-year bank refinance at 5.5 percent yields $760 payments, compared to $850 on a personal loan at 9 percent. Eligibility tilts toward bank options for those with $50,000+ income, since personal lenders cap debt-to-income at 36 percent stricter. And although both erase federal forgiveness paths, bank versions preserve cosigner releases quicker, with 80 percent processed within 30 days.

Turns out, tax implications favor neither outright, as interest deductibility caps at $2,500 annually for qualified student loans only before refinance; post-swap, personal loans lose that edge entirely. Observers have seen hybrid approaches work, like partial bank refinancing for federal portions while pivoting privates personally, netting 15 percent overall savings in case studies.

Risks, Regulations, and Real-World Case Studies

Regulatory oversight varies: U.S. banks fall under FDIC rules mandating clear disclosures, while personal lenders adhere to CFPB guidelines that cap fees and require ability-to-repay checks; in Canada, pivots face FCAC scrutiny on high-cost credit, banning rates over 35 percent. Risks include credit dings from inquiries (5-10 point drops temporary) and loss of deferments, but data shows scores rebound within six months for 90 percent of users.

Consider one case where a recent grad swapped $30,000 at 6.5 percent via bank deposit; payments fell to $550 monthly from $720, saving $4,200 over five years, although the borrower missed Public Service Loan Forgiveness eligibility. Another pivoted to a personal loan amid job loss, locking a fixed rate but facing 4 percent fees that offset initial gains. Experts who've tracked these note that April 2026's rate environment favors refinancing now, with forecasts predicting 0.5 percent hikes by year-end.

It's noteworthy how apps from banks like Ally integrate refinancing simulators, projecting exact savings, whereas personal platforms emphasize prequalification without hard pulls first. People often find that while pivots suit short-term fixes, bank routes build long-term banking loyalty with perks like cashback on payments.

Navigating Trends and Future Outlook

April 2026 brings fresh dynamics, as European Central Bank policies influence global rates, pushing U.S. student refinances below 5 percent for primes; Australian data from ASIC reveals 12 percent uptake in pivots amid housing crunches. Those studying trends predict AI-driven approvals will cut processing to hours, with banks leading via account data analytics.

So, borrowers weigh speed against security, with bank refinancing dominating for volumes over $25,000 per LendingTree aggregates. Yet personal options persist for gig workers lacking banking ties, offering 24/7 applications.

Key Takeaways and Strategic Choices

Bank account refinancing delivers lower rates and seamless integration for established customers, while personal loan pivots provide unsecured access and quick funds for others; figures confirm 25-35 percent savings potential either way, contingent on timing and credit. Data underscores shopping multiple offers, as variances span 3 percent APRs. Ultimately, those decoding debt swaps align choices with income stability and loan sizes, ensuring swaps propel toward payoff without hidden pitfalls.