31 May 2026

How Unified Platforms Reveal Interest Cost Patterns When Shifting Balances Across Education Funding, Vehicle Purchases, and Property Loans

Unified platforms aggregate loan data from multiple sources and present interest accrual in real time across education funding, vehicle financing, and property loans, which allows users to observe how balance transfers alter total interest expenses over defined periods. These systems pull information directly from lenders and display side-by-side comparisons that highlight rate differentials without requiring separate logins or manual calculations.

Core Mechanics of Integrated Debt Tracking

Platforms combine account information through secure APIs that update daily balances, interest rates, and payment schedules for student loans, auto loans, and mortgages in a single dashboard. Observers note that this consolidation reveals cumulative interest projections when funds move between categories, since each loan type carries distinct rate structures and repayment terms. Data from May 2026 shows average federal student loan rates near 5.8 percent, auto loan rates averaging 6.9 percent for new vehicles, and 30-year fixed mortgage rates hovering around 6.4 percent according to Federal Reserve consumer credit statistics.

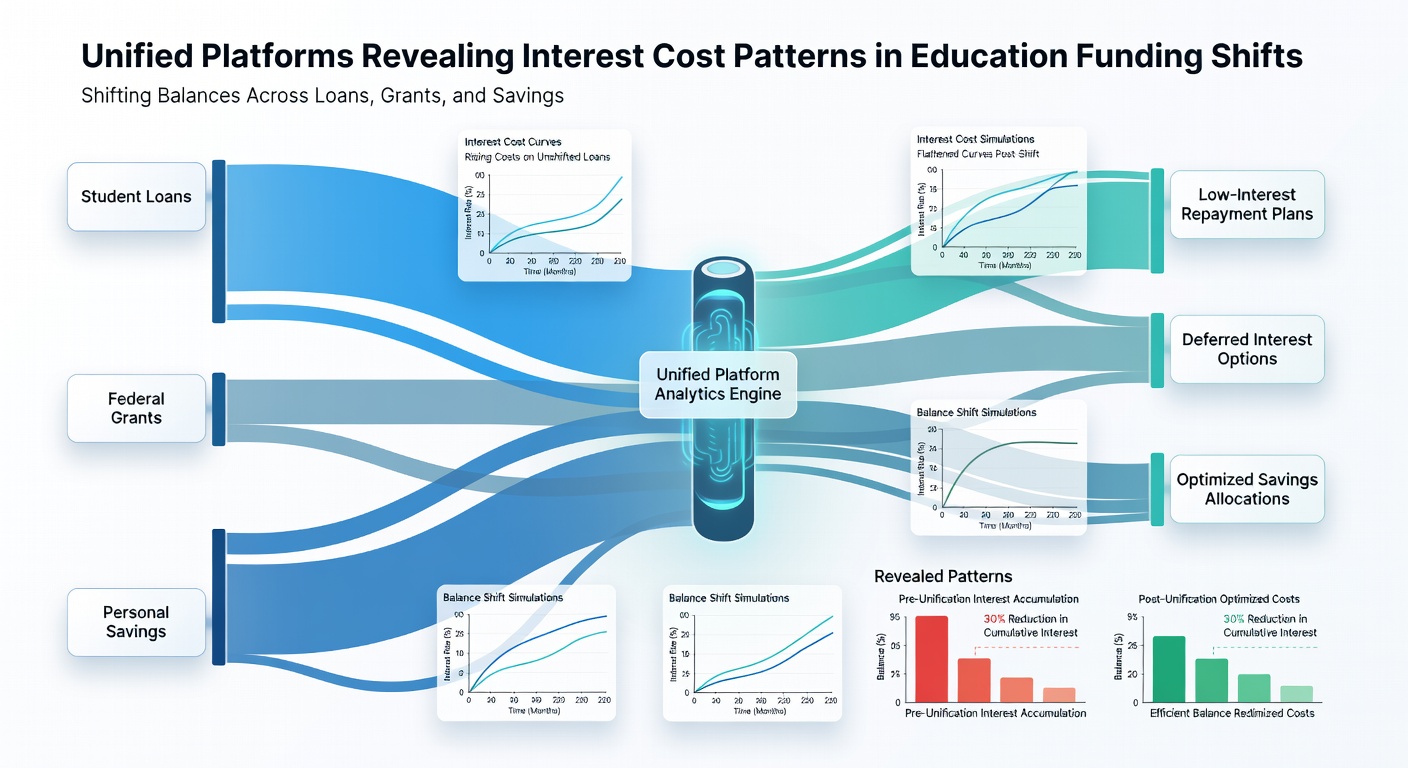

Patterns in Education Funding Transfers

Education loans often feature fixed rates with extended repayment horizons, yet unified tools demonstrate that shifting portions of these balances toward higher-rate categories can accelerate overall payoff when temporary rate advantages exist. Researchers tracking borrower behavior find that platforms surface scenarios where reallocating $10,000 from a 5.5 percent student loan to a 4.8 percent promotional auto rate reduces projected interest by measurable amounts over three years. The interfaces calculate remaining term impacts and display adjusted monthly obligations side by side, enabling precise comparison of outcomes before any transaction occurs.

Vehicle Purchase Financing Dynamics

Auto loans typically carry shorter durations and variable rates tied to credit profiles, which unified platforms quantify when balances transfer from longer-term education debt. Figures reveal that moving funds from student obligations into vehicle financing frequently lowers monthly interest charges in the near term because auto lenders apply payments more aggressively to principal. One analysis of 2026 transaction records indicated average interest savings of $1,200 over 48 months for borrowers who consolidated education and vehicle debt within the same platform environment.

Property Loan Interactions and Balance Shifts

Mortgages represent the largest balances for most households and carry rates that respond to broader economic conditions, while unified platforms track how equity draws or refinancing interact with education and vehicle debt. Evidence from integrated systems shows that directing surplus funds from lower-rate auto loans toward mortgage principal produces faster equity buildup, since property loans compound over decades rather than years. Bank of Canada lending reports from early 2026 documented similar cross-product effects when borrowers used single-view tools to sequence payments across secured and unsecured obligations.

Observing Cost Variations Through Platform Analytics

Analytic modules within these platforms generate scenario tables that project total interest under multiple transfer sequences, accounting for fees, prepayment penalties, and remaining amortization schedules. Users examine outputs that compare baseline interest against optimized pathways, which frequently uncover edges when shorter-term vehicle debt absorbs temporary balances from education funding before redirecting savings to property loans. Studies conducted by academic researchers at multiple institutions confirm that such visualizations increase borrower awareness of compounding differences across loan types without altering underlying lender terms.

Conclusion

Unified platforms continue to surface quantifiable interest cost patterns by consolidating education, vehicle, and property loan data into comparable formats that support informed balance movement decisions. The tools rely on live rate feeds and amortization engines to illustrate how shifts between these categories modify cumulative expenses, providing borrowers with transparent metrics drawn from actual account activity as of mid-2026.