Inside 0% Balance Transfer Credit Cards: How They Stack Up Against Personal Loans for Debt Relief

19 Apr 2026

Inside 0% Balance Transfer Credit Cards: How They Stack Up Against Personal Loans for Debt Relief

Unpacking 0% Balance Transfer Credit Cards

Those carrying high-interest credit card debt frequently seek out 0% balance transfer cards as a lifeline, allowing them to shift balances to a new card with no interest for an introductory period that often stretches 12 to 21 months; data from the Consumer Financial Protection Bureau (CFPB) reveals that millions of Americans use these offers annually to pause interest accrual while they chip away at principal. Card issuers like Chase, Citi, and Discover roll out these products, typically charging a one-time balance transfer fee of 3% to 5% of the amount moved—say, $300 on a $10,000 transfer—yet that upfront hit often pales against ongoing APRs hovering around 20% or more on existing cards. What's interesting is how eligibility hinges on credit scores above 670 for prime offers, since issuers scrutinize FICO scores and debt-to-income ratios before approving limits high enough to consolidate meaningful debt.

And while the 0% window shines bright, the reality sets in post-promo when standard rates kick back up to 18-29%, turning any leftover balance into a costly burden unless payments accelerate during the grace period; experts who've tracked user outcomes note that only about 40% of transfers fully pay off before expiration, per Federal Reserve studies on consumer credit behavior.

The Mechanics of Balance Transfers in Action

Picture someone with $15,000 spread across three cards at 22% APR; they apply for a 0% intro card, get approved for a $20,000 limit, and transfer the balances within the first 60 days to snag the promo rate, paying that 4% fee but slashing monthly interest from roughly $275 to zero. Payments then flow directly to principal, potentially clearing the debt in 18 months with $900 monthly outlays; but miss the transfer deadline or exceed the promo terms, and interest compounds retroactively on some cards, a pitfall the Australian Securities and Investments Commission (ASIC) warns about in its consumer guides. Observers point out that promotional periods have lengthened in recent years, with top offers hitting 21 months as of April 2026 amid competitive banking pressures, although fees crept up slightly to offset issuer costs.

Now, tracking multiple cards adds complexity—apps from issuers help monitor promo end dates—but those who consolidate aggressively often emerge debt-free faster than sticking with originals, according to analyses from credit bureaus like Equifax.

Personal Loans Enter the Debt Relief Arena

Personal loans for debt consolidation offer a lump-sum payout to clear credit cards, replaced by fixed monthly payments over 24 to 84 months at rates from 6% to 36%, depending on borrower profiles; lenders like SoFi, LightStream, and banks such as Wells Fargo dominate this space, where data indicates average rates sat at 11.5% for qualified borrowers in early 2026, per LendingTree reports. Unlike revolving credit, these unsecured loans (or sometimes secured against assets) demand full repayment on a set schedule, freeing up credit lines once paid off but tying borrowers to the term regardless of early prepayments—most allow penalty-free extras, though. Eligibility broadens slightly here, with scores as low as 580 qualifying for subprime rates, although prime borrowers snag the lowest APRs; figures from the Federal Reserve show personal loan originations surged 15% year-over-year into April 2026, fueled by refinancing waves amid stabilizing inflation.

Take a $15,000 loan at 8% over 36 months: monthly payments land around $485, totaling about $2,500 in interest versus $8,000 if lingering on 22% cards; that's where the rubber meets the road for long-haul debt fighters who prefer predictability over promo gambles.

Head-to-Head: Costs, Terms, and Eligibility Breakdown

Interest and Fees: The Real Money Mover

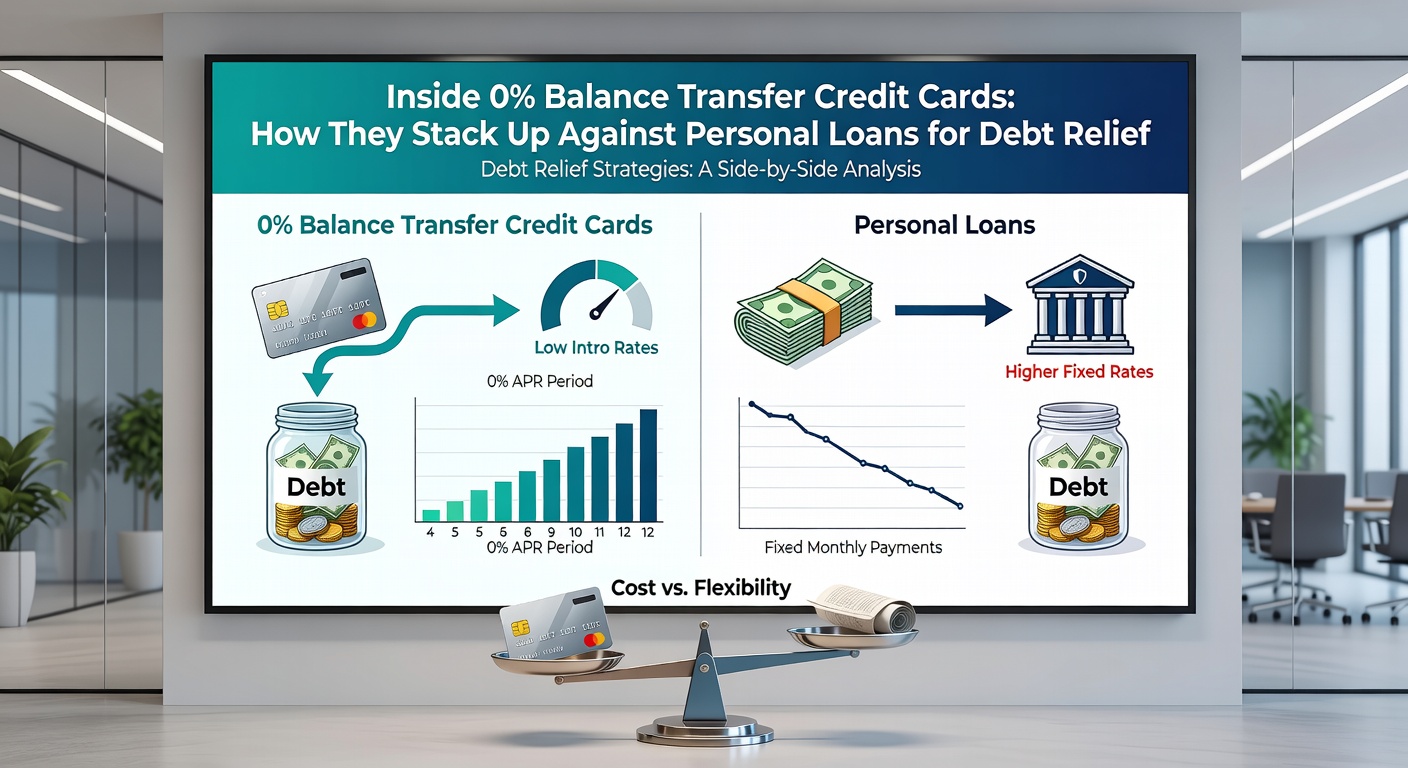

Zero percent cards win short-term with no interest during promos, but personal loans edge out on total cost for larger debts or longer horizons; researchers at the Urban Institute crunched numbers showing a $10,000 transfer at 3% fee and 18-month 0% pays $300 upfront if cleared fully, whereas a 7% loan over five years adds $3,200 total interest—yet the loan avoids post-promo spikes that trap 60% of card users, per CFPB complaint data. Fees stack differently too: cards hit with 3-5% transfers plus potential annual charges ($0-95), while loans bake origination fees (1-8%) into the principal but skip ongoing balances.

Repayment Flexibility Versus Structure

Balance transfers tempt with minimum payments as low as 1-4% monthly, letting people stretch but risking promo expiry; personal loans enforce fixed amounts, pushing faster equity buildup since extra payments shave principal without interest recalculation. But here's the thing: cards demand discipline to max minimums during 0%, or debt balloons; loans automate the process, ideal for those who falter on self-pacing, as behavioral finance studies from universities like Harvard reveal.

Who Qualifies and Credit Impact

Prime credit (670+) unlocks best 0% cards with high limits, but dings scores temporarily from new inquiries and utilization jumps; personal loans forgive slightly lower scores yet scrutinize income more, with hard pulls lingering 12 months on reports. Observers note cards preserve liquidity—no new debt pile—while loans consolidate into one payment, simplifying budgets for households juggling multiples.

Pros, Cons, and When Each Shines

0% cards excel for disciplined short-term crushers eyeing quick wins under $20,000, boasting no fixed term to bind cash flow; drawbacks loom in expiry cliffs and fee layers that bite overspenders. Personal loans suit bigger loads or shaky habits, locking rates amid April 2026's 5.25% Fed funds environment where variable card APRs chase benchmarks upward; yet they extend timelines, accruing more interest if life derails extras. Case in point: one study from the National Bureau of Economic Research followed cohorts where card users saved 25% more interest short-term but defaulted twice as often post-promo compared to loan takers.

People who've stacked both often hybridize—transfer small balances for 0% speed, loan the rest for stability—although issuers cap transfers at account limits, complicating mixes.

Market Snapshot: April 2026 Trends

As of April 2026, top 0% offers from U.S. Bank and Bank of America push 20-month intros at 3% fees, while Canadian lenders via the Financial Consumer Agency of Canada (FCAC) mirror with 15-18 months amid tighter regs; personal loan rates dipped to 10.8% averages for excellent credit, per Bankrate surveys, thanks to softening inflation. EU players like those under the European Central Bank oversight offer similar consolidations, but U.S. dominates volume with 25% origination growth. That's notable because rising minimum payments on cards force shifts, handing loans a volume edge for debts over $25,000.

Yet digital platforms innovate: apps now simulate outcomes, projecting payoff dates side-by-side; those tools, gaining traction, help users dodge traps like teaser rates masking high reversion APRs.

Navigating Choices with Eyes Wide Open

Debt relief seekers weigh timelines against discipline levels, running calculators to model scenarios; cards turbocharge short sprints for the committed, while loans pave steady marathons for most. Data underscores hybrids or singles tailored to debt size—under $10k favors cards, above leans loans—ensuring minimums align with budgets. Ultimately, pre-qualifying across issuers reveals personalized fits, turning overwhelming options into actionable paths forward.

Conclusion

Balance transfer cards and personal loans both carve paths from high-interest traps, each leveraging 0% intros or fixed rates to reclaim financial footing; as April 2026 markets evolve with longer promos and competitive lending, borrowers who compare fees, terms, and approvals stack the odds for savings. Researchers emphasize running personalized math first—total interest, payoff speed, credit ripple—since one size rarely fits all debt profiles. Those who match tools to habits clear balances efficiently, emerging with healthier scores and breathing room; the key lies in reading fine print and committing to the plan that sticks.