19 May 2026

Mapping APR Patterns: How Rate Calculators Guide Shifts Between Credit Card Debt and Mortgage Adjustments

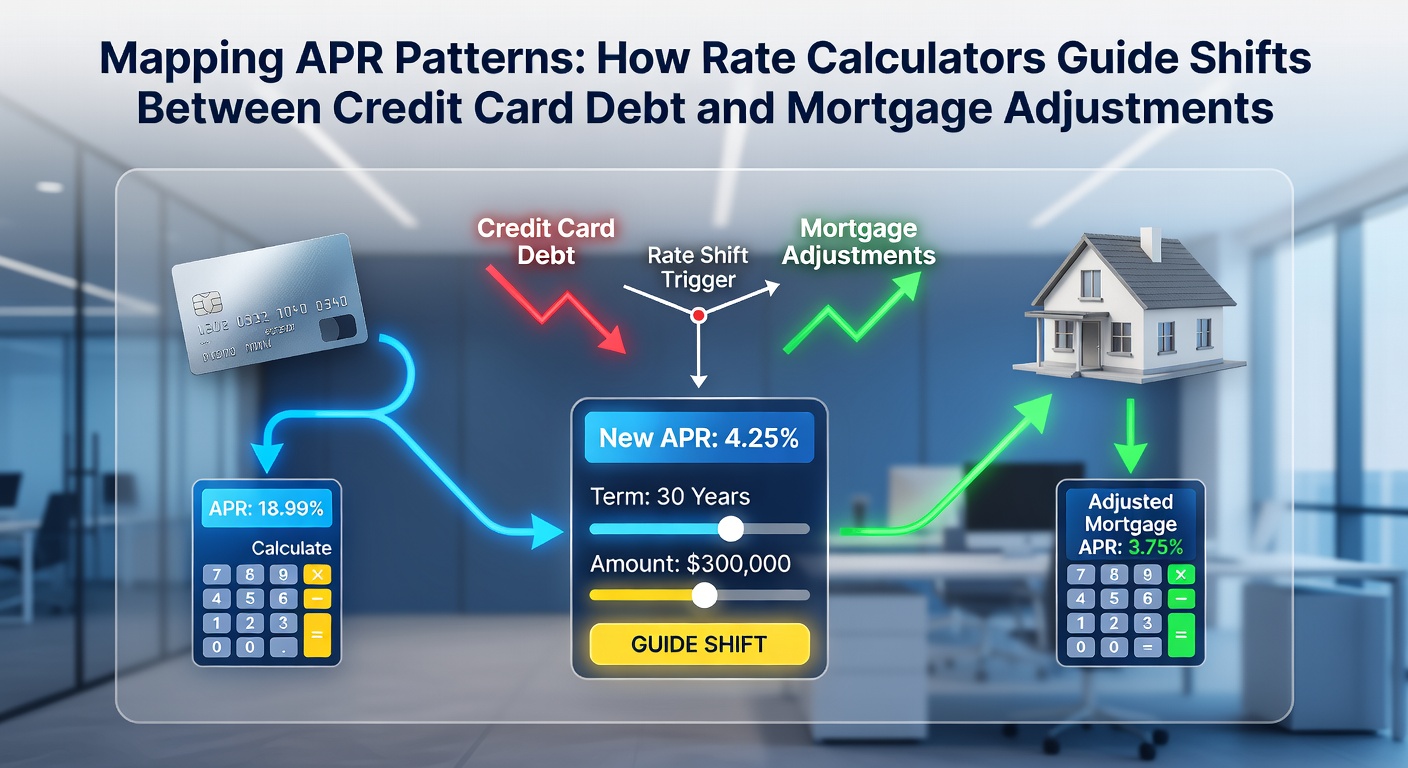

Rate calculators serve as essential tools for tracking patterns in annual percentage rates across credit card balances and mortgage products, allowing precise evaluations of when debt shifts become viable based on current market conditions. Financial analysts observe that these calculators process inputs like outstanding balances, interest terms, and repayment timelines to highlight opportunities where high-APR credit card debt might transfer into adjusted mortgage structures with lower effective costs.

Core Mechanics of APR Comparison Tools

Rate calculators operate by aggregating data on variable and fixed rates, then projecting total interest expenses over specified periods while factoring in fees and amortization schedules. Users input details such as current credit card APRs that often range from 15 to 25 percent depending on credit profiles, alongside mortgage rates that typically fall between 3 and 7 percent in major economies. The tools then generate side-by-side projections that reveal crossover points where refinancing or home equity adjustments could reduce overall payments.

Patterns emerge clearly when calculators incorporate historical rate trends, showing how credit card APRs tend to fluctuate with central bank policies more rapidly than mortgage benchmarks. In practice, these systems flag scenarios where sustained high card rates exceed mortgage thresholds by certain margins, prompting structured evaluations of lump-sum transfers or line-of-credit draws against property equity.

Shifts Between Credit Card Balances and Mortgage Frameworks

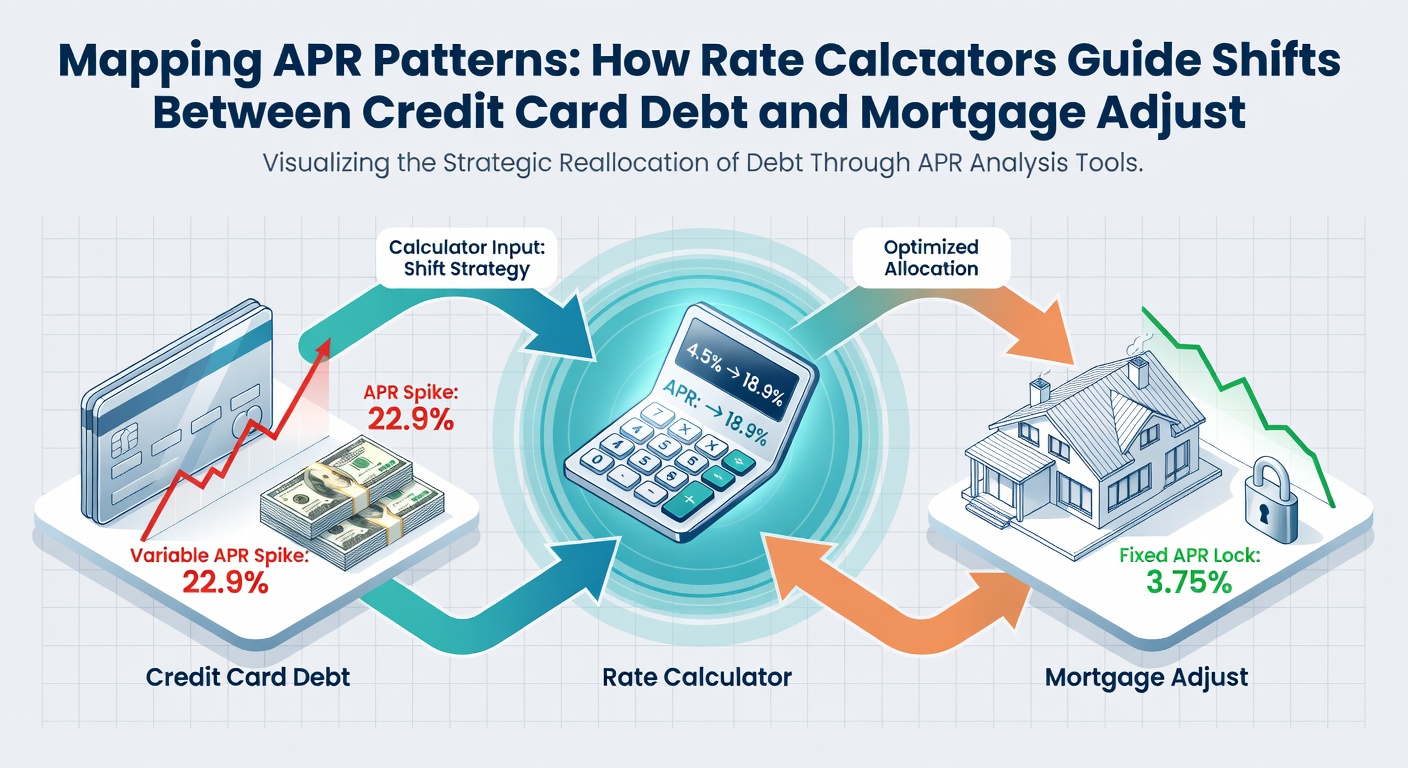

Observers note distinct mapping patterns when rate calculators compare revolving credit card debt against fixed or adjustable mortgage terms. Credit card debt carries immediate compounding effects that accelerate balances, whereas mortgage adjustments often allow extended amortization that spreads costs. Calculators quantify these differences by modeling scenarios such as a $15,000 card balance at 22 percent APR versus incorporation into a mortgage at 4.5 percent over 15 years, yielding measurable differences in cumulative interest.

Data from May 2026 indicates average credit card APRs in the United States held near 21.4 percent while 30-year mortgage rates averaged 4.8 percent, according to Federal Reserve reports. Similar patterns appear in Canadian markets where Bank of Canada figures placed variable mortgage rates around 5.1 percent amid credit card averages near 19.8 percent. Calculators help map these gaps by simulating prepayment penalties, closing costs, and equity requirements that influence net savings from any shift.

Practical Applications in Debt Restructuring

Those who study financial behavior find that individuals apply rate calculators during periods of rate stability or anticipated changes, such as post-policy announcements from major central banks. The tools guide decisions by calculating break-even timelines where interest savings offset transaction fees involved in mortgage adjustments. For example, one documented case involved a household using calculator outputs to shift $28,000 in card debt into a cash-out refinance, resulting in projected reductions of monthly outflows by approximately 35 percent over five years.

Researchers have identified recurring patterns where calculators highlight risks like extended loan durations that increase total interest despite lower rates. These systems often include sensitivity analyses for rate changes, showing how a 1 percent rise in mortgage benchmarks could alter the viability of debt consolidation moves. European Central Bank data from early 2026 further illustrates regional variations, with eurozone mortgage averages near 3.9 percent contrasting against credit card rates exceeding 16 percent in several member states.

Calculators also incorporate tax implications and insurance adjustments that accompany mortgage modifications, providing layered outputs that go beyond simple rate comparisons. Patterns indicate stronger incentives for shifts when credit card utilization rates exceed 30 percent of available limits, as calculators demonstrate accelerated interest accrual under those conditions. Industry reports emphasize the role of real-time data feeds that update projections as market rates move throughout the year.

Emerging Trends in Calculator-Driven Strategies

Analysts track how digital rate calculators integrate with personal finance platforms to automate pattern recognition across multiple debt types. Users receive alerts when mapped APR differences reach predefined thresholds, facilitating timely reviews of mortgage adjustment options. Studies from academic sources reveal that households engaging these tools complete shifts more frequently during spring months when seasonal rate reviews align with tax filing periods.

What's interesting is how calculators account for credit score impacts from new mortgage inquiries versus existing card management, offering balanced views of long-term financial positioning. Data shows consistent use among borrowers with mixed debt portfolios, where tools project scenarios involving partial transfers rather than full consolidations to preserve equity buffers.

Conclusion

Rate calculators continue to map APR patterns by delivering structured comparisons that inform decisions on moving between credit card debt and mortgage adjustments. Evidence from regulatory and central bank sources demonstrates their utility in quantifying savings potential while highlighting associated costs and timelines. As markets evolve, these tools maintain relevance through updated data integration that reflects current rate environments across regions.