21 May 2026

Seeing the Full Picture: How All-in-One Banking Apps Help Spot Rate Advantages Across Student, Auto, and Home Borrowing

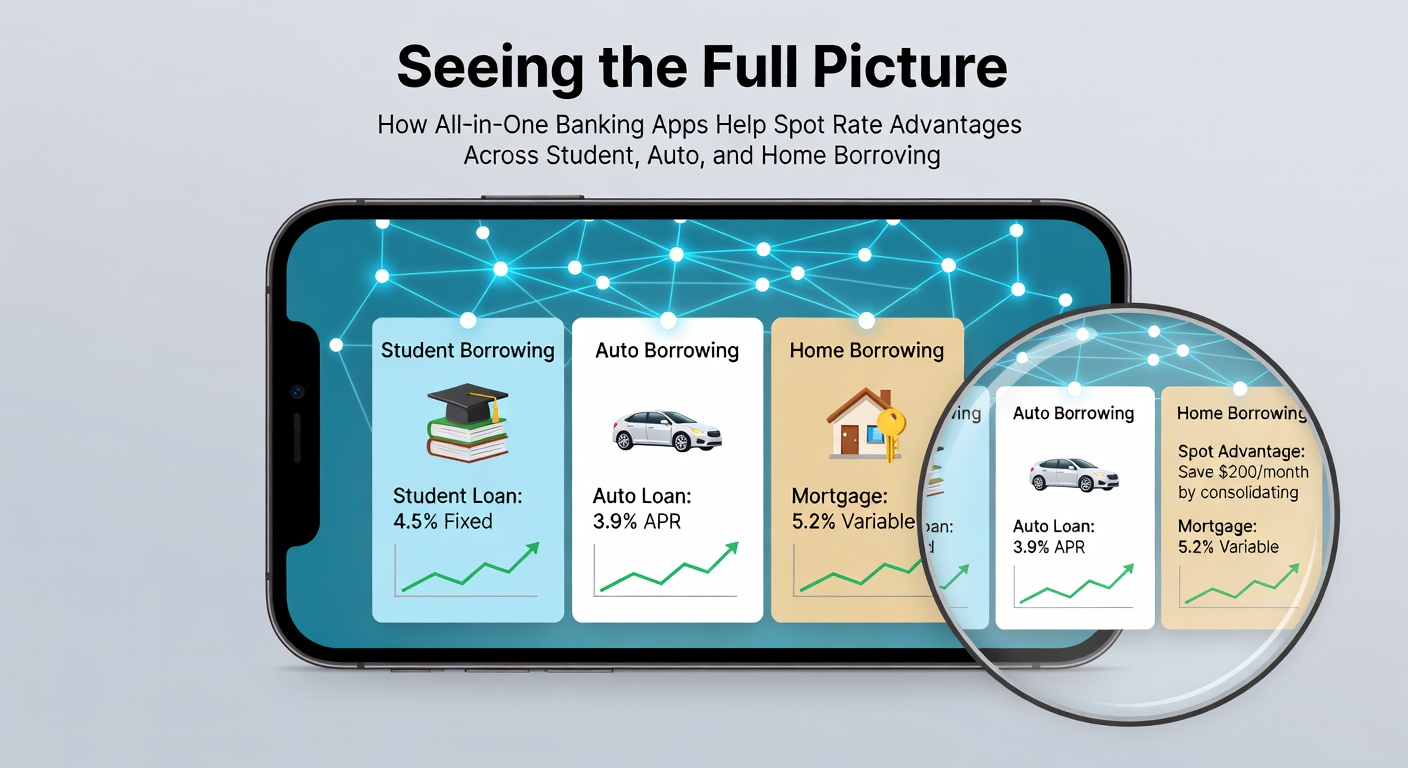

Banking applications that consolidate multiple financial services into single platforms now track borrowing rates across student loans, auto financing, and home mortgages in ways that separate tools rarely match. Users gain access to unified dashboards where current offers appear side by side, allowing direct comparisons without switching between lender websites or spreadsheets. Data from May 2026 shows average student loan rates holding near 6.8 percent for federal options while private lenders posted figures between 5.9 and 7.4 percent depending on credit profiles, according to Federal Reserve reports.

These platforms pull real-time information from linked accounts and credit bureaus, then surface opportunities when rates shift. Someone managing both an existing auto loan at 8.2 percent and a student debt balance can view proposed refinance figures for each within the same screen, which highlights potential savings from moving one or both obligations. Integration features reduce the manual work of checking individual sites, and alerts notify users when a lender adjusts its offerings overnight.

Consolidated Views Across Loan Categories

Applications designed for comprehensive money management display student debt alongside vehicle financing and property loans because rate environments often diverge. Federal student rates remained fixed through spring 2026 while auto loan averages climbed toward 7.1 percent in several regions. Home mortgage figures, by contrast, fluctuated with bond yields and sat around 6.3 percent for 30-year terms. Observers note that seeing these numbers together helps borrowers recognize when one category offers clearer advantages than others.

Users connect their existing accounts once, after which the app aggregates balances, payment histories, and qualifying criteria. The system then runs comparisons against current market listings without requiring repeated logins elsewhere. This setup proves useful when someone qualifies for a lower rate on a home equity line yet still carries higher-interest auto debt that could benefit from refinancing elsewhere.

Rate Tracking and Alert Systems

Built-in monitoring tools scan multiple lenders daily and flag changes that meet user-defined thresholds. Someone who set an alert for auto rates below 6.5 percent receives a notification when a credit union posts a new promotion, complete with qualification details pulled from the borrower's linked profile. Similar triggers operate for student loan refinancing and mortgage adjustments, which keeps scattered opportunities visible in one place.

Research from the Bank of Canada indicates that borrowers who review rates across categories every two weeks identify refinance windows 23 percent more often than those checking lenders individually. The same study found that integrated platforms shorten the time between spotting a favorable rate and submitting an application because pre-filled forms already contain verified income and credit data.

Practical Examples of Cross-Category Decisions

Take one borrower who carried $24,000 in student loans at 6.9 percent, a car loan at 8.4 percent, and a mortgage at 6.1 percent in early 2026. After linking everything to a single app, the platform highlighted a personal loan offer at 5.8 percent that could replace the auto balance while leaving the mortgage untouched. The borrower also saw a student loan refinance option at 5.7 percent from a credit union partner. Because both figures appeared together, the decision process focused on total monthly savings rather than isolated product details.

Another case involved a homeowner whose equity had grown enough to support a cash-out refinance at 5.9 percent. The app compared that rate against keeping the original mortgage and using a separate home equity loan, then cross-referenced the results with current auto and student rates to show net interest cost differences over five years. Such side-by-side calculations rely on the app's ability to import live balances and apply consistent assumptions across products.

Data Sources and Market Context in 2026

Market conditions in May 2026 reflected steady federal funds rates alongside regional variations in consumer lending. Student loan refinancing activity increased 14 percent year over year as private lenders competed for borrowers with strong credit scores, while auto rates remained sensitive to used-vehicle inventory levels. Mortgage spreads narrowed slightly in urban markets but stayed wider in rural areas. All-in-one platforms incorporate these variables through feeds that update multiple times daily, giving users access to localized offers rather than national averages alone.

Industry reports from the European Banking Authority highlight similar patterns in cross-border lending comparisons, where borrowers using unified apps encountered rate differences of up to 1.2 percentage points across equivalent products. The ability to view such spreads without leaving one interface supports more informed allocation of refinancing efforts among student, auto, and home obligations.

Conclusion

All-in-one banking applications continue to evolve their comparison tools by incorporating broader data sets and faster update cycles. Borrowers who maintain multiple loan types gain visibility into relative advantages when rates move, which supports decisions based on combined interest costs rather than single-product analysis. As of late spring 2026, these platforms already handle millions of linked accounts and deliver alerts that align with observable market shifts across student, auto, and home borrowing categories.